A U.S. state is moving to crack down on some of the financial risks that can come with the rising popularity of Buy Now, Pay Later offers.

On Thursday, Illinois Gov. JB Pritzker signed legislation aimed at protecting people who take out Buy Now, Pay Later (BNPL) loans from hidden charges, unaffordable loans, purchase disputes and other risks.

Illinois follows California and New York, which have similar laws in place.

It comes as soaring costs have left many consumers turning to Buy Now, Pay Later plans to buy essentials like groceries and with the cost of living continuing to bite.

The Illinois law caps BNPL loans at the 36 per cent rate cap that already exists for other lenders in the state. It also requires lenders to carry out “reasonable risk-based underwriting and to consider the borrower’s ability to repay the loan.”

For context, credit card companies in Canada typically charge between 19 and 21 per cent interest.

The law also grants BNPL borrowers the same rights as credit card holders in cases of disputes or payment errors.

Lenders in Illinois can no longer require you to set up automatic payments for Buy Now, Pay Later plans. They are also prohibited from attempting to debit a bank account for the second time if the account has insufficient funds.

“Strong protections for Buy Now, Pay Later loans are important, especially as these loans are being used for everyday expenses like groceries and are being pitched for vital necessities such as rent,” said Lauren Saunders, senior attorney at the U.S.-based National Consumer Law Center (NCLC).

Get breaking National news

Get breaking Canada news delivered to your inbox as it happens so you won’t miss a trending story.

Buy Now, Pay Later plans have become “ubiquitous” for many purchasers, Saunders said.

According to research from Morgan Stanley, Buy Now, Pay Later loans financed two per cent of all e-commerce sales in 2020.

By 2024, that was up to six per cent.

Canadians are coming to rely on it more and more, too.

Typically, consumers have used Buy Now, Pay Later for big purchases like TVs, laptops and other expensive electronics.

But research suggests Canadians are dipping into these services for small purchases such as takeout.

In August 2025, Canadian fintech firm Koho, which allows users to split repayments for purchases they have already made, said the share of eligible users using that option has risen from 38 per cent to 44 per cent in the last six months.

The top categories for which Canadians used Buy Now, Pay Later at Koho were groceries, telecom and restaurants. Based on a sample size of 10,000 users, the average transaction was $187, and the average loan amount was $345.

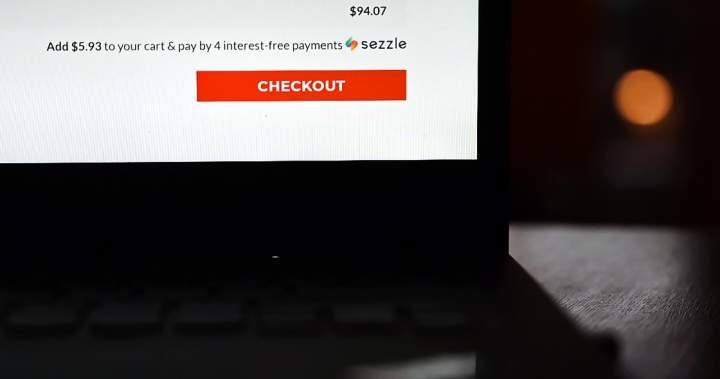

Using Buy Now, Pay Later plans can “make purchases look cheaper than they are,” the National Consumer Law Center (NCLC) says on its website.

“(Some) BNPL companies tout the credit as interest free. But some lenders charge late fees, bounced payment fees, and other fees, which can add up to the equivalent of a high annual percentage rate (APR),” the website says.

Unlike a credit card, which typically has a single payment due once a month on a predictable date, Buy Now, Pay Later purchases can have multiple payments due in a single month.

“BNPL providers typically require consumers to authorize automatic debits to their bank account or credit card. If the bank account does not have sufficient funds, the payment may trigger a negative balance and an overdraft fee or nonsufficient funds (NSF) fee,” NCLC adds.

“Borrowers should keep in mind why they are taking out a BNPL product — is it for convenience or more breathing room in the budget?” said Stacy Yanchuk Oleksy, CEO of not-for-profit credit counselling agency Money Mentors.

Borrowers should come with a repayment plan, she added.

“BNPL products are neither good nor bad, it’s how they are used that can make it good or bad for our finances, so use them cautiously and one at a time,” Oleksy said.

What is the law in Canada?

Canada’s regulatory framework around Buy Now, Pay Later plans is a patchwork of provincial rules, with some calls for stricter rules as these loans grow more popular.

In Ontario, for example, NDP MPP and consumer protection critic Tom Rakocevic has called for the creation of a consumer protection framework for Buy Now, Pay Later in the province.

The Consumers Council of Canada and ACORN (Association of Community Organizations for Reform Now) Canada have both called for “consistent law, regulation and standards” to protect people from falling into “debt traps, higher costs and exploitation.”

Federally, the Financial Consumer Agency of Canada (FCAC) “does not set interest rates for financial products.”

“Setting interest rates remains a business decision for lenders, subject to applicable federal and provincial laws, including the Criminal Code,” a spokesperson for the federal agency told Global News.

However, the agency ensures that banks comply with federal laws and regulations. This includes obligations around disclosure, minimum grace periods and express consent.

“That could also apply to loans that federally regulated financial institutions provide as a BNPL product,” the spokesperson said.

PakarPBN

A Private Blog Network (PBN) is a collection of websites that are controlled by a single individual or organization and used primarily to build backlinks to a “money site” in order to influence its ranking in search engines such as Google. The core idea behind a PBN is based on the importance of backlinks in Google’s ranking algorithm. Since Google views backlinks as signals of authority and trust, some website owners attempt to artificially create these signals through a controlled network of sites.

In a typical PBN setup, the owner acquires expired or aged domains that already have existing authority, backlinks, and history. These domains are rebuilt with new content and hosted separately, often using different IP addresses, hosting providers, themes, and ownership details to make them appear unrelated. Within the content published on these sites, links are strategically placed that point to the main website the owner wants to rank higher. By doing this, the owner attempts to pass link equity (also known as “link juice”) from the PBN sites to the target website.

The purpose of a PBN is to give the impression that the target website is naturally earning links from multiple independent sources. If done effectively, this can temporarily improve keyword rankings, increase organic visibility, and drive more traffic from search results.